Monthly Mortgage Update: September 2013

Summer is coming to an end. Temperatures are falling, but mortgage rates are rising!

(Sorry, bad joke.)

Let’s keep this analogy going, though. Much like the unpredictable weather we’ve seen all across Canada this summer, it’s been a similarly erratic season in mortgages.

Mortgage Rates Continue to Rise

Last month finished with the best 5-year fixed mortgage rates hovering around 3.20%. Now, the best rate listed in Ontario is nearly 20 basis points higher at 3.38%. To put that in perspective, you would now pay around $3,150 more interest over five years at the higher rate, at the average home price in Canada of $382,273 in July 2013 (using a 10% down payment and 25-year amortization).

Variable mortgage rates, on the other hand, have stayed put (at around 2.50% for a 5-year term) and look increasingly attractive. In a special for the Financial post, Garry Marr pointed out that the spread (difference) between fixed and variable rates is moving closer to historical norms, as studied by brainy York University Prof. Moshe Milevsky.

While that may be true, the mortgage qualifying rate has also moved up 20 basis points to 5.34%; this is the rate used by lenders to qualify borrowers seeking mortgages with variable rates or terms of less than five years.

Why are Mortgage Rates Rising?

Mortgage rates follow government bond yields with a strong correlation, and bond yields have risen recently so mortgage rates have followed. Furthermore, it’s possible the recent CMHC securitization cap – discussed in more detail in this blog post – could also be contributing to the increase in mortgage rates.

Under the National Housing Act Mortgage-Backed Securities (NHA MBS) program, banks are able to securitize and sell large portions of the mortgages they carry on their books for a lower cost than they otherwise could, because the securities are backed by the CMHC. The lower cost of funding for banks gets passed onto homebuyers in the form of lower mortgage rates. However, there is now a cap on CMHC backing, which limits big lenders access to lower cost funding.

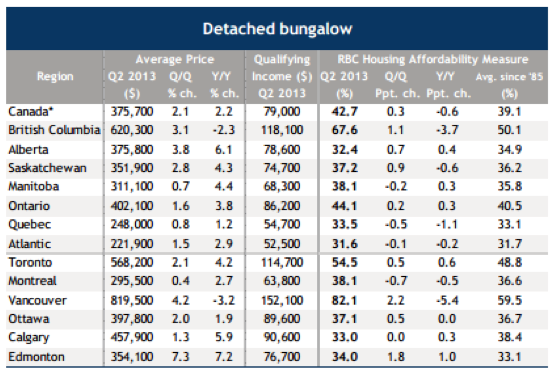

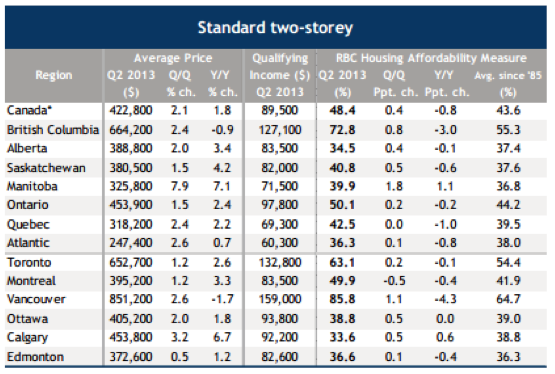

Housing Market is Resilient

The housing market continues to be resilient, despite higher mortgage rates and declining affordability. RBC released its quarterly housing affordability report this month, which revealed Canada’s two most unaffordable cities – Toronto and Vancouver – have become even less affordable. In fact, in two of the three categories of homes RBC measures (bungalows and two-storey homes), affordability has fallen across Canada as whole from the previous quarter. This means Canadians are paying more of their pre-tax income to service their homes.

Despite the affordability gap, prices and sales are increasing in Toronto, Vancouver and the nation.

Ratehub.ca News

Hot Off the Press!

Alyssa, Ratehub.ca’s CEO, made her primetime debut this month on CTV, appearing not once but twice in mortgage news segments. I think she’s a natural!

Ratehub.ca was also featured in The Wall Street Journal, Global News, The Huffington Post, the Toronto Star and on Chinese television this month! We may not speak Mandarin, but clearly our reach crosses language barriers.

We’re Hiring!

We continue our hiring spree and are looking for talented PHP Developers. If you know any, refer them over and collect $500 buckeroos!

New Mortgage Sections

We’ve added some new sections to our Education Centre – Bad Credit and Second Mortgages, Investment Properties and a Condominium Buyer’s Guide – so be sure to check them out.

We pride ourselves in providing high-quality educational content and these new sections do not disappoint.

RateHubber Pro Money Tips Facebook Series

We’re still running our RateHubber Pro Money Tips Facebook series and have released some great quotes from 20 of the top personal finance experts in Canada. Check back every Monday and Wednesday for a new tip!

‘Til next month!

–KL

Kerri-Lynn (KL) is the Chief Marketing Officer at Ratehub.ca. Her mortgage recaps can be found monthly on our blog.