GICs vs. Low-Cost Index Funds

Investors are constantly faced with choices. And one of the biggest dilemmas individuals encounter is where to place their hard-earned money. If you ask most people, they’ll probably say they want the best return for the lowest risk. Of course, generally speaking, the potential for higher rewards usually comes with the possibility of loss. By contrast, investments with very little risk tend to offer the smallest returns.

In this post, we’ll compare two possible investments: GICs and low-cost index funds. As a reminder, index funds track the performance of a major market, such as the Toronto Stock Exchange. And whereas mutual funds often come with annual fees of 2.00% or more, index funds are much more cost effective, in the 0.2-1.0% annual range.

The Case for GICs

Why choose the GIC route? The major advantage with GICs is that your capital is guaranteed. There are two layers of guarantee: first, by the financial institution that issued it, and second, by government deposit insurance if the bank happens to fail (highly unlikely but you’re covered in case it happens).

GICs also pay a set amount of interest, which over time means your investment will grow. If you hold a GIC for many years, you have the opportunity to accumulate compound interest (interest on interest), growing your initial capital even more.

The Case for Index Funds

How about index funds? Whereas GICs are primarily savings tools (i.e. protecting your money), index funds that track the stock market are more concerned with growing your capital. Unlike GICs, your initial investment in an index fund is not guaranteed. However, the potential to grow your capital is much higher. This happens in two ways: the market may increase in value and/or you could receive dividend payments.

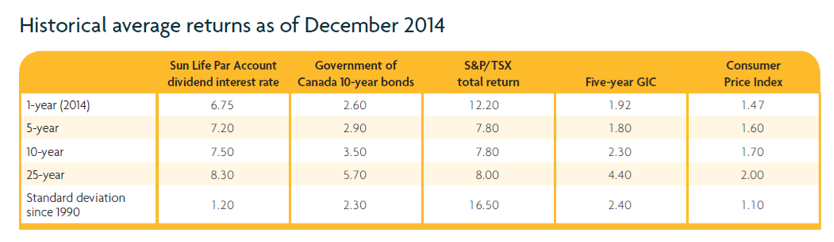

You’re probably wondering how GICs and index funds compare historically. As the following chart from Sun Life shows, over the past 25 years, the TSX has returned an average of 8.00% per year vs. 4.40% for a 5-year GIC.

The outperformance of the TSX last year was even greater: 12.20% vs. 1.92% for a 5-year GIC.

In a sense, the recent outperformance of index funds is related to the low rates offered by fixed income products like GICs. Because interest rates are so low, investors are increasingly favouring assets like the stock market, due to the potential for better returns.

Gone are the days when you could buy a GIC and earn 5% risk-free. Indeed, the 25-year average return of the GIC in the Sun Life chart is just that, an average. When you look at the 5-year return for the GIC, it is much, much less.

Source: Sun Life

So is it case closed? The index funds win by a country mile? Not necessarily.

It’s true that GICs right now do not offer much in the way of return. Sure, you do get some interest, but it’s not huge.

If there’s a case to be made for GICs, then, it’s not that you’ll make a lot of money buying them. Rather, as stock markets have surged since the depths of the financial crisis, the potential for equity prices to decline as increased. Very few experts believe stocks are undervalued, whereas many now say we’re in an equity bubble. If this is the case, markets could decline in coming years.

Let’s imagine that an index fund happens to decline by 10% in the following year vs. the nearly 8% it’s returned over the past 5 years. In this scenario, a GIC paying somewhere on the order of 1.50% seems like a great deal by comparison.

This isn’t to say you should attempt to “time” the market”, just that if equity prices do decline, a GIC may actually turn out to be a better investment than it currently appears.

Flickr: Sarah Sosiak